- 22 Oct 2025

- Elara Crowthorne

- 22

Thailand Crypto Tax Calculator

Calculate Your Tax Liability

Based on Thailand's 2025-2029 crypto tax rules for domestic residents and foreign entities

Enter Your Transaction Details

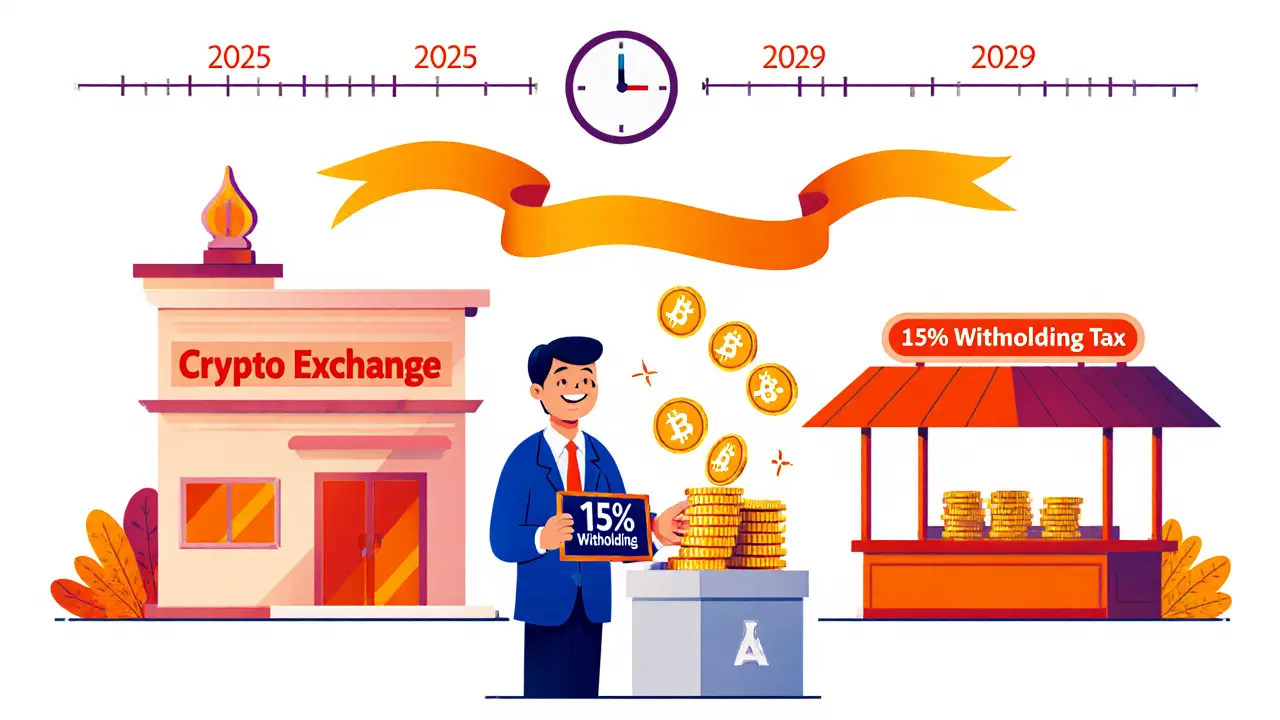

If you’ve heard talk about a "15% gains tax" on crypto in Thailand, you’re probably mixing two very different rules. The reality is that Thailand now offers a 5‑year personal income tax exemption for crypto capital gains on approved exchanges, while a separate 15% withholding tax still applies to foreign entities earning crypto income in the country.

Why the confusion matters

Understanding the split between the domestic exemption and the foreign withholding tax can save you from costly mistakes. Mis‑reporting a tax‑free gain as taxable (or vice‑versa) can trigger penalties from the Thai Revenue Department.

What the law actually says

Thailand cryptocurrency tax is governed by Ministerial Regulation No. 399 (B.E. 2568), published in the Royal Gazette on 5 September 2025 and effective from 1 January 2025 to 31 December 2029. The regulation creates a five‑year personal income tax exemption for capital gains earned from the sale or transfer of digital tokens, but only when the transaction occurs on a SEC‑licensed digital asset exchange that is authorized by the Thai Securities and Exchange Commission.

Before this exemption, crypto gains were taxed like any other capital gain, ranging from 0% to 35% depending on the taxpayer’s total annual income. Companies faced corporate income tax rates up to 20%.

Who benefits from the 5‑year exemption?

- Thai residents who trade on a licensed exchange or broker.

- Individuals (not companies) who realise profit from buying and selling crypto tokens.

- Investors who can prove that every trade happened on a platform listed in the SEC’s registry.

The exemption does not cover earnings from:

- Unlicensed platforms, including international exchanges.

- Peer‑to‑peer (P2P) sales, decentralized exchanges (DEXs), or DeFi swaps.

- Staking rewards, lending interest, or derivative contracts.

For those excluded activities, regular personal income tax rates still apply.

The 15% withholding tax - who pays it?

Separate from the domestic exemption, Thailand imposes a 15% withholding tax on crypto income earned by foreign entities. This rule applies when a non‑resident company provides crypto‑related services within Thai jurisdiction, such as operating a crypto exchange platform for Thai users.

The withholding tax is deducted at source and remitted to the Thai Revenue Department, meaning the foreign entity receives net proceeds after the 15% is taken off.

Key limitations you must watch

Even with the exemption, the Thai Revenue Department expects meticulous record‑keeping. You’ll need to:

- Log every transaction date, amount, and exchange used.

- Separate qualifying trades (on SEC‑licensed platforms) from non‑qualifying ones.

- Calculate net gains or losses for each tax year.

- Report the exempted portion on your personal income tax return, just to document compliance.

Failure to differentiate can lead to a retroactive tax assessment on the entire gain.

Practical tax‑planning tips

- Trade only on approved platforms. Verify the exchange’s SEC licence before opening an account.

- Consider timing gains to fall within the exemption window (2025‑2029). Gains realised after 31 December 2029 will be taxed under the standard rates.

- Use tax‑loss harvesting: sell under‑performing assets to offset gains from qualifying trades.

- Keep a separate ledger for DeFi activities, staking, or P2P sales-they remain taxable.

- Consult a Thai‑qualified tax adviser if you have mixed activities (both exempt and taxable).

Side‑by‑side comparison

| Aspect | Domestic Residents (Qualified Trades) | Foreign Entities |

|---|---|---|

| Tax rate on capital gains | 0% (exempt for 2025‑2029) | 15% withholding at source |

| Applicable platforms | SEC‑licensed exchanges/brokers only | Any platform serving Thai market, but tax withheld |

| Reporting requirement | Declare exempted gains on personal return | Withholding tax filed by payer; entity may claim credit |

| Other crypto income (staking, lending) | Taxed as ordinary income (rates 0‑35%) | Subject to standard corporate tax (up to 20%) |

What the future could hold

Deputy Finance Minister Julapun Amornvivat expects the exemption to spur about $1 billion in annual economic activity. The policy is set to expire at the end of 2029, and the government has said it will review the framework based on market response. Keep an eye on any proposed extensions or new guidelines, especially around DeFi and staking, which are still gray areas.

Quick checklist before you file

- Confirm your exchange has a valid SEC licence.

- Export transaction history (CSV) for the entire tax year.

- Separate exempt and taxable activities.

- Calculate net capital gains for exempt trades.

- Include a note on your personal tax return that the gains are covered by Regulation 399.

Frequently Asked Questions

Do I still need to file a tax return if all my crypto trades are exempt?

Yes. You must still file a personal income tax return and state that the gains are covered by the 5‑year exemption. This provides a paper trail in case the Revenue Department asks for proof.

Can I use an overseas exchange and still claim the exemption?

No. Gains from unlicensed or foreign platforms are outside the exemption and are taxed at your marginal personal rate.

What happens after 31 December 2029?

The exemption ends, and capital gains will be subject to the standard progressive rates (0%‑35%). The government may introduce a new regime, so stay tuned.

Is staking income taxed?

Current guidance treats staking rewards as ordinary income, so they fall under the regular personal tax brackets.

How does the 15% withholding tax affect a foreign crypto exchange operating in Thailand?

The exchange must deduct 15% from any Thai‑sourced crypto revenue before remitting it to the foreign parent. The foreign entity can claim a credit in its home‑country tax filing, depending on double‑taxation agreements.

Bottom line: the 15% figure you’ve heard about isn’t a universal gains tax - it’s a specific withholding rule for non‑residents. Thai residents trading on approved platforms enjoy a full tax exemption until 2029, but they must stay disciplined about record‑keeping and platform choice. Miss one of those steps, and the exemption disappears fast.

22 Comments

🚀🚨 TL;DR: Thailand's crypto tax landscape splits into a 5‑year exemption for SEC‑licensed exchange trades and a 15% withholding on foreign‑entity revenues. Stay on approved platforms, keep meticulous ledgers, and you’ll dodge the bite. 📊💡

It’s reassuring to see policy that actually rewards disciplined investors, especially when the exemption encourages long‑term planning rather than speculative frenzy. By treating crypto like any other asset, the Treasury is nudging us toward responsible stewardship.

Stop wafflin’ over the fine print – if you’re tradin’ on an unlicenced exchagne you’re just askin’ for a tax audit. The law ain’t a suggestion, it’s a mandate, so get your records straight or face the penalty.

Great overview! Just a reminder: the exemption only covers capital gains, not staking or lending income. Those still fall under the regular personal tax brackets, so keep those streams separate in your spreadsheet.

They’re setting us up – the 15% withholding is a trap to funnel Thai crypto money straight into foreign banks while the locals get a “free” exemption that could vanish any day. Keep an eye on the next amendment, it won’t be pretty.

For anyone still figuring out the paperwork: start by exporting your trade history from the SEC‑licensed exchange in CSV format, then flag each row with a “Qualified” tag. Summarize net gains per fiscal year and attach the Reg‑399 reference on your Roth‑IRP filing.

Use only approved platforms – no foreign exchanges – and you’ll stay in the exemption zone

Oh sure, because everyone loves filling out extra forms just to prove they didn’t break a rule that most people didn’t even know existed. 🙄 Just slap a note on your return and hope the tax guy believes you.

The Thai tax exemption framework, while seemingly generous, demands a disciplined approach to record‑keeping that many casual traders tend to overlook.

First, every transaction must be timestamped with the exact date, amount, and the identifier of the SEC‑licensed exchange used, which means you should pull detailed CSV reports at least quarterly.

Second, you need to categorize each trade as either “qualified” or “non‑qualified,” a distinction that becomes critical when you reconcile your yearly summary.

Third, the calculation of net capital gains should aggregate all qualified buys and sells, subtracting any transaction fees, to arrive at a clean figure that can be reported as exempt.

Fourth, even though the gains are exempt, the Thai Revenue Department still requires you to list them on your personal income tax return as a matter of transparency.

Fifth, any income derived from staking, DeFi yields, or peer‑to‑peer sales must be isolated in a separate ledger because those streams remain fully taxable.

Sixth, consider employing tax‑loss harvesting strategies by deliberately selling under‑performing assets within the exemption window to offset gains from other qualified trades.

Seventh, maintain backups of all exchange statements, blockchain explorer screenshots, and any communication that verifies the platform’s SEC licensing status.

Eighth, if you operate across multiple exchanges, ensure that you do not inadvertently mix qualified and non‑qualified trades in the same accounting period.

Ninth, be aware that the exemption expires on 31 December 2029, after which all capital gains will revert to the progressive personal tax rates ranging from 0 % to 35 %.

Tenth, the government has hinted at reviewing the policy post‑2029, so stay tuned for potential extensions or new compliance obligations.

Eleventh, consulting a Thai‑qualified tax adviser early can save you from costly re‑filings, especially if you have a hybrid portfolio that includes both exempt and taxable activities.

Twelfth, remember that foreign‑entity withholding tax of 15 % applies only when a non‑resident company provides services to Thai users, so individual traders are generally insulated from that rate.

Thirteenth, keeping a clear audit trail not only protects you from retroactive assessments but also positions you advantageously should you ever seek to demonstrate compliance to international partners.

Finally, the key to unlocking the benefits of Regulation 399 lies in consistency, documentation, and a proactive mindset toward the evolving regulatory landscape.

Dear fellow investors, I urge you to adopt a systematic approach to your Thai crypto compliance; by adhering to the prescribed record‑keeping protocols, you safeguard both your financial interests and the integrity of the emerging market.

Fantastic news for Thai traders!!! Keep those records tight and enjoy the tax‑free window!!!

Got the memo the exemption only works on licensed exchanges keep it simple and don’t miss the deadline

Honestly I feel like I’m missing out when everyone talks about tax exemptions and I can’t help but wonder if I should be more involved in the crypto scene; maybe I’ll start tracking my trades more closely because I don’t want to feel left behind; the whole thing just makes me anxious about missing paperwork; I wish someone would just do it for me; it’s like a weight on my shoulders; I keep thinking about the numbers and I can’t stop; the exemption sounds great but the effort feels huge; I just want to relax and watch my portfolio grow without the stress; maybe I’ll ask a friend for help; I’ll try to set reminders; it’s all a bit much.

While many celebrate the five‑year break, I’d wager the government will slip in a retroactive clause once the market balloons-best to stay skeptical.

Let’s pool our experiences: I’ve found that tagging each CSV row with a color code-green for qualified, red for taxable-makes the year‑end reconciliation a breeze and encourages community members to share templates.

Oh, marvelous-another regulatory nuance to memorize. Because what we really needed was more paperwork to keep us on our toes.

Watch out! The 15% withholding could be a front for funneling money to off‑shore accounts-be extra cautious!!!

The Thai government’s move to protect domestic investors showcases national pride; foreign entities should respect our sovereignty and comply without complaint.

Is it not tragic that a nation’s attempt to foster innovation is shackled by tax shadows? Like a phoenix, our crypto community must rise above bureaucracy.

Everyone says it’s just a tax thing but really it’s a way for the state to control crypto flow and keep the big players in check.

In the grand tapestry of finance, taxes are the invisible threads that bind us; perhaps this exemption is a test of our collective vigilance.

May I respectfully inquire whether the Thai Revenue Department provides a standardized template for reporting exempted crypto gains, and if so, where might one obtain the official documentation?